18 Months back my wealth manager sold me a financial instrument. It was a structured product from Deutsche Bank and was linked to the growth of the Stock Index. While there was no written commitment I was assured of returns that would be much higher than a bank FD – lots of upside , no downside – I was promised. Last month I got my money back – but not a paise in gain. Input 10 Lacs – Output 10 Lacs. During the 18 month period the Nifty did go up – Deutshe Bank made money , Axis Bank made money , my wealth manager made her incentive – and I was left looking like a sucker. (If I had put this money in a FD I would have made ~ 1.5 Lacs in Pre Tax profit)

Ever wondered how Banks / Wealth Managers make money. What funds the fancy offices and hefty bonuses ? They have no manufacturing , IP , Code, product to sell ? Why is it that they promise a lot but never commit even 1 % more than a bank FD ?

The harsh truth is they make money out of you. Insurance policies , Complicated Structured products , the stock market itself – are all designed smartly to ensure that the retail investor is attracted but very soon left high & dry. The head of Wealth Management of a large bank told me that 90% of retail investors lose money in the Market. After 20 years of stock market investing I tend to agree with him – whether in the US or in India you gain big & lose big but Nett Nett if you do not have tremendous discipline its difficult to make money in the stock market.

So the next question is where do you invest ? How do you beat inflation ? India’s gross domestic savings rate has increased near-steadily over the Five-Year Plans and is among the highest in the world ( Nearly 35%) . The recent savings rate of the country is comparable to Indonesia, Thailand and Korea but much lower than that of China, Malaysia and Singapore. (Consumer states like the US and the UK had their savings rate as low as 11% levels in 2009, while the rate is 17% for France and 21.4% for Germany. Among emerging economies, Brazil had a low savings rate at 16.5%.)

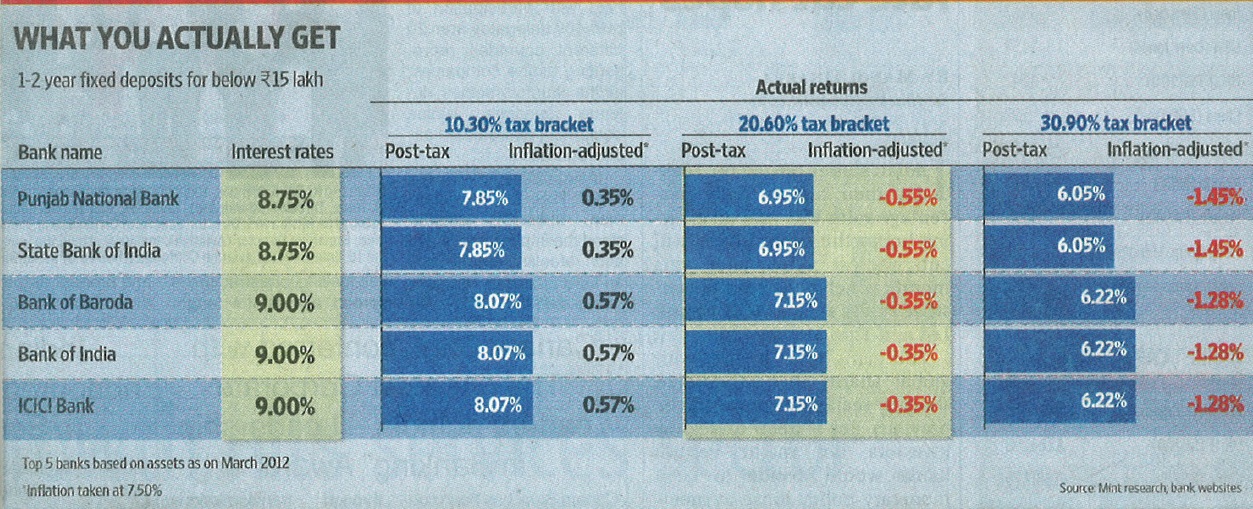

Lets look at simple FD – its easy to understand , easily available in every branch , has high liquidity. If you see the table below for people in the 30% Tax Bracket your FD interest rate does not help you beat Inflation !

Talking of Tax – most of us think we pay 30 % Tax – but we pay a lot more. There is service tax on everything you buy , add education Cess , Metro Cess and inflated prices on Petrol – we probably end up paying 10 – 15 % on everything we buy – so our actual Tax Liability is much higher than 30%.

Real Estate has got expensive. 10 years back when you bought a new flat you paid Registration on the undivided share of land only. Today you pay on the entire flat value – add to this the Service Charges & VAT on construction – you actually pay close to 20% of property value in Taxes & Registration. Builders take away most of the profit and appreciation is limited.

Making money has indeed become difficult in the last few years . Which brings me back to the question of what are the options to beat Inflation – I see a few of them.

1. Debt Funds – which should hopefully give 10% + Post Tax returns if the RBI governor starts cutting Interest rates

2. Land – yes its not Liquid and requires a lot of research to get a clean deal – but with population growing and mass exodus to Metro’s difficult to lose money on good land deals.

3. Gold – Not so sure on this one. Looks like it will crash. But given the wealth and black money that exists in this country the demand for Gold may not drop and with india being one of the biggest markets for Gold globally – it may keep shining for many years. But this is virtual profit – because no indian family sells Gold for cash at a profit ( not many Jewelers give you cash too ) – they either hoard it trade it for newer jewellery , or loan it to Muthoot finance.

4. Maybe buy the Index ( Nifty-bees) – because from a long term you can go wrong on individual stocks or mutual funds – but its very difficult to beat the Index. That may be the simple and safe way to 12% annualized returns.

Well said VAK! Many a times the wealth advisers are searching for money in our house. It is day light robbery. He makes money for sure and we make only if we are lucky. If we are unlucky we may even loose. By the time you wanted to check what is the reason you get a call from him saying i am in a different bank and with better product.

LikeLike

You forgot to mention that the index funds and debt funds were also suggested. and you were convinced on the same by your wealth manager only.. Also the biggest reason for loss is lack of patience and discipline in investment.

fear and greed drive investors.

LikeLike

Hi VAK, got this link from my wife who had written to you earlier on some visa tips and referred me here since I am an investor.

I cannot agree more that the wealth manager makes money off your principal and your returns than make money off your returns

I still do not understand why the manager assured you you will get FD returns? What was in the structure that gave him the confidence and you the comfort?

Having said that, I feel equities are the best way to grow your wealth, and like you say investing in the Index is the best way to go for a passive investor – less tension and reasonable returns! Since the index was introduced Nifty has delivered 14.5% pre-dividend, so an fund that tracks it closely will give similar returns over long periods.

Lastly these investments are exempt from tax long term and that is another returns booster.

Warm regards,

Kimi

LikeLike